Analysis: fall in LNG prices prompts call for Papua New Guinea mini-Budget

The impact of the fall in LNG prices since the 2015 Budget was prepared in October last year warrants a mid-year mini-Budget, according to prominent economist Paul Flanagan.

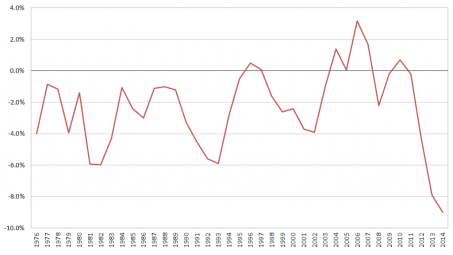

PNG Budget Balances (% of GDP) 1976-2014

The former Australian Treasury and Papua New Guinea Treasury advisor has analysed the PNG Treasury’s 2014 Final Budget Outcome and the central bank’s March Monetary Statement.

He says it shows the government’s medium-term financial plan is off track, and a ballooning deficit requires a mini-budget to deal with the problem.

‘Just as the Australian government is having to deal with the impact of lower commodity prices, so too is the PNG government.’

The potential impact of the fall in LNG revenue is revealed in the March Monetary Policy Statement and without action, there is also a potential risk to the country’s balance of payments and foreign reserves, he told Business Advantage PNG.

‘Just as the Australian government is having to deal with the impact of lower commodity prices, so too is the PNG government,’ he says.

Deficit

Economist Paul Flanagan

‘The major concern is that the budget deficit, which has been running at the second highest level in PNG’s history in 2013, and the highest ever in PNG in 2014, clearly are not sustainable.’

The 2013 deficit of a then historic high of 7.7% of Gross Domestic Product was planned to drop to 5.9% in 2014. This target has been missed, and the official deficit is recorded as 7.3%, he says.

‘More worryingly, the underlying fiscal deficit is now 9.0% of GDP – the highest in PNG’s history since Independence.

‘The major concern is that the budget deficit, which has been running at the second highest level in PNG’s history in 2013, and the highest ever in PNG in 2014, clearly are not sustainable.’

‘These deficits build up debt, put pressure on the balance of payments, build up interest rates, and they make foreign exchange scarcer because the government is spending a lot more money on imports.

Resources income

Flanagan says plans to put income from the country’s resources, such as the PNG LNG project, into the planned Kumul Holdings concept or the Savings Fund of the Sovereign Wealth Fund, should now be delayed until the deficit is paid off.

‘The highest rate of return the government of PNG can get from any monies invested through a savings fund, a SWF, or investments in Kumul, the highest guaranteed financial return you can get, is through paying off your debt and lowering your interest costs.

‘Those interest costs for the government have more than doubled in the last 18 months.’

‘When you are hit with such a large external shock to what is your key export earner, you have to be flexible. You’ve got to be ready to respond.’

The Budget Outcome report shows domestic borrowing jumped from the K1,708 million estimated in the original budget for 2014 to K2,983 million. PNG’s interest costs jumped from K486 million in 2013 to K953 million in 2014.

While Flanagan believes the government should sell its shares in Oil Search, which were bought for K2.9 billion with a loan from UBS, he says it will not help the budget bottom line, because the value of those shares has dropped by K400 million.

But it’s better to take the hit now, he says, and bring those loan interest rate payments back to the budget, which are higher than the dividend income.

Mini-Budget

‘To be fair to the government, it was not clear when the Budget was being prepared last October just how big the fall in oil prices would be.

‘But when you are hit with such a large external shock to what is your key export earner, you have to be flexible. You’ve got to be ready to respond.

‘And that’s why a mini-Budget coming out now to deal with that loss in revenue is also a chance to set out more realistic funding levels for government priorities in future years.’

Paul Flanagan is a Visiting Fellow at the Centre, which is based at the Australian National University, Canberra. His full analyses can be found here and here.