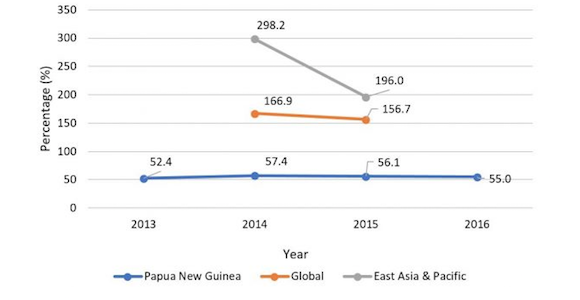

PNG microfinance loan-to-deposit ratio compared with East Asia (grey) and globe (yellow). Source: Devpolicy

The form of microfinance services we see today is largely derived from the community-based mutual credit transactions that existed centuries ago and that were based purely on trust and non-collateral borrowings and repayments.

The first microfinance service in Papua New Guinea was introduced by the Asian Development Bank (ADB) in 2002 under the Microfinance and Employment Project.

Today, microfinance services in PNG are supplied through the state-owned National Development Bank, five licensed microbanks, 21 savings and loans societies (SLS) and around 70 small community-based non-government organisations.

While these financial institutions have successfully reached out to more than 43,000 microcredit borrowers and 250,000 depositors in PNG over the years, the microfinance industry has been facing the problem of disproportionately low demand for borrowings in comparison to savings deposits since inception.

Data prepared by the Microfinance Information Exchange (MIX) shows that the loan-to-deposit (LTD) ratio of PNG’s microfinance industry ranged from 52 to 58 per cent between 2013 and 2018.

This implies that, for every kina deposited in a microfinance institution (MFI) in PNG, only 55 toea are lent out as a loan to the public.

Loans-to-deposits

Devpolicy’s Dek Joe Sum.

The LTD ratio is usually used as a measure to evaluate the liquidity and financing structure of a financial institution, and to determine whether it is capable of self-funding or requires external financing.

While there is no general rule of thumb for where the optimal LTD ratio lies, the MFIs in PNG have been experiencing a much lower LTD ratio than the global and regional average standard over the years.

The East-Asia and Pacific region, which comprises 136 MFIs in 14 countries (including PNG), has a track record of issuing loans at least two times the value of deposits in 2014 and 2015.

More importantly, PNG remains the only country in the region with a LTD ratio of less than one. This implies that there may be excessive liquidity in the country’s MFIs that is not fully utilised for loan purposes.

Self sufficiency

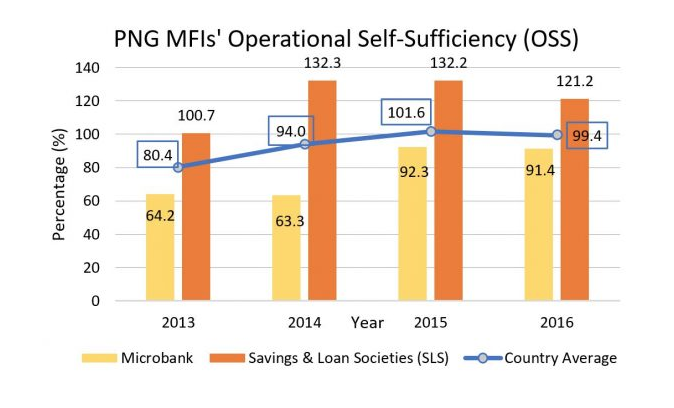

Operational self-sufficiency (OSS) is a measure used to evaluate microfinance institution sustainability. It assesses the ability of a financial institution to cover its operational and financial expenses with its revenues.

The data in the second figure shows that the country’s microfinance institutions on average just barely achieved self-sufficiency, at 101.6 per cent and 99.4 per cent in 2015 and 2016 respectively.

‘Microcredit … is the only channel whereby people living in poverty can gain access to extra money (credit) for personal use and wealth creation’

While all five savings and loan societies in the survey sample recorded more than 100 per cent self-sufficiency, the micro-banks on average have not been able to. This implies that, on average, the revenues received by the micro-banks are not large enough to cover their expenses.

This result is not surprising given that the savings and loan societies only issue loan products exclusively to their members and have few branches.

The micro-banks, on the other hand, experience high operational costs associated with providing services to the general population by setting up branches and establishing financial agents in the most rural and remote regions of the country.

Microfinance Institutions’ operational self sufficiency. Source: Devpolicy

Demand

The situation faced by the micro-banks could be improved with an increase in the demand of loans from the population.

As most of the unutilised funds from the surplus of deposits over loans are used to invest in government and treasury bills, with returns ranging from 4.7 per cent (182-day T-bill) to 8.0 per cent (364 day T-bill), the microfinance institutions could have easily earned much more by issuing more loans at a higher interest rate.

‘PNG’s banking and financial sector has the lowest loan-to deposit ratio of any country in the Pacific.’

The ongoing low LTD rate in the institutions certainly decreases the effectiveness of what microfinance can do to help the poor.

While there are many different services covered under the umbrella term of microfinance, such as micro-insurance and micro-leasing, microcredit undoubtedly forms the core of microfinance, as it is the only channel whereby people living in poverty can gain access to extra money (credit) for personal use and wealth creation.

Wealth creation

Lower demand for microcredit among rural and low-income households leads to lower wealth creation.

This prevailing problem is not only impeding efforts to reduce poverty effectively, it is also hampering the government’s initiatives to promote growth in local business ownership and expand the country’s tax base.

It is important to note that the low LTD ratio is a sector-wide problem and does not only affect the microfinance industry.

In fact, PNG’s banking and financial sector has the lowest LTD ratio of any country in the Pacific. The PNG government needs to develop a more comprehensive policy to address the lack of lending in the country.

Financial incentives such as an interest rate cap or the use of less stringent collateral requirements may not be sufficient or may even be counterproductive.

Rather, the government needs to improve the business environment in PNG so that the general population is able to develop bankable projects. Increased demand for credit and greater lending will then follow.

Dek Joe Sum is Associate Lecturer and Project Coordinator at the Australian National University’s Development Policy Centre. He is currently working in Port Moresby. This article first appeared on the devpolicy blog.