Opinion: Is Papua New Guinea’s kina really depreciating?

Amid fears of further declines in the value of Papua New Guinea’s currency, the kina, economists Bobby Kunda and Stephen Howes analyse how the kina has been performing against all its key trading currencies – and come to some surprising conclusions.

Lae port. Credit: ICTSI

There is lots of talk these days about currency depreciation in Papua New Guinea. And the kina did fall by 5.5 per cent against the US dollar over the course of last year, and by 9 per cent since 2018.

But the USD is only one currency.

The Trade Weighted Index (TWI) gives an idea of how the kina is behaving against all the currencies of the countries with which PNG trades. The Bank of Papua New Guinea (BPNG) calculates the TWI, but with a lag of some six months or more. The most recent data from BPNG is currently from June 2023, and so is out of date.

In this article, we calculate more recent TWI values and find that the TWI is almost the same as it was at the start of 2023, and the same as in 2018.

PNG’s trading currencies

BPNG provides daily exchange rates for 19 currencies with a lag of a month or less. Trade data from 2022 is available for all of them except Kuwait and can be used to weight the bilateral exchange rates to update BPNG’s June TWI. The greater the value of trade, the greater the weight assigned to the currency. The trade shares add up to about 95 per cent of total exports and imports.

‘For all the talk about it, on a trade-weighted basis there was actually only very modest depreciation last year.’

Australia is the most important trading partner, with a share of 25 per cent, followed by China with 19 per cent, Singapore with 17 per cent and Japan with 14 per cent.

We don’t know the exact formula used by BPNG to calculate the TWI, but, using a standard formula, we are able to closely replicate it.

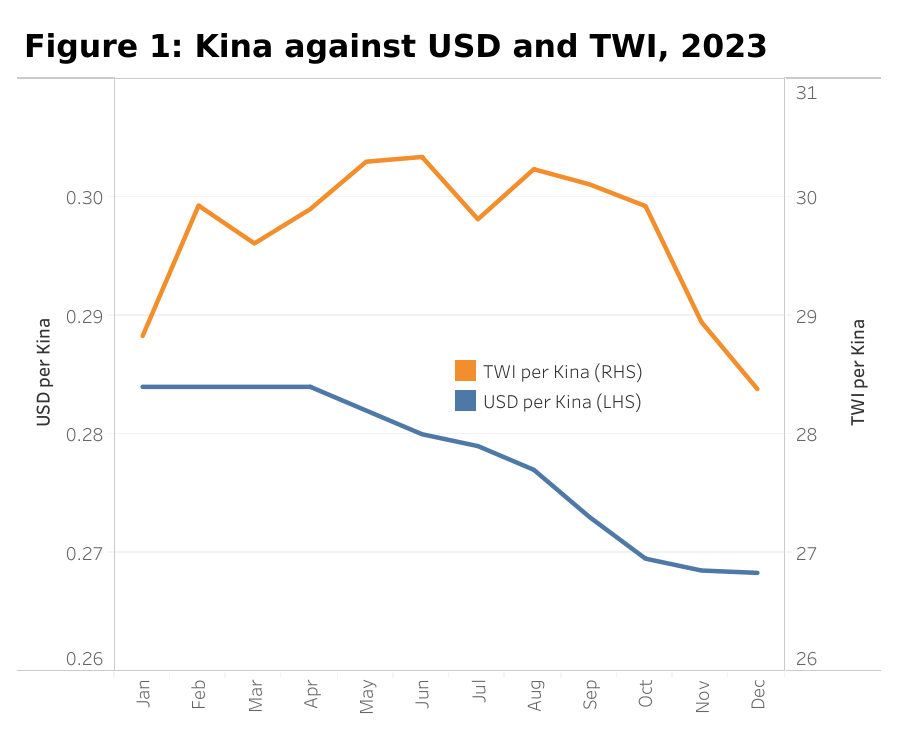

The graph below shows for every month in 2023 the USD/kina, as reported by BPNG, and the TWI, as reported by BPNG up to June 2023 and as calculated by us since then.

Whereas the kina fell against the US dollar by 5.5 per cent, from 28.4 cents in January 2023 to 26.8 cents in December 2023, against the TWI it only fell by 1.6 per cent over the same period: from 28.83 in January to 28.38 in December.

This is because the US dollar has been strengthening against nearly all currencies, not just the kina.

Notes: Exchange rate values are for the last day of each month.

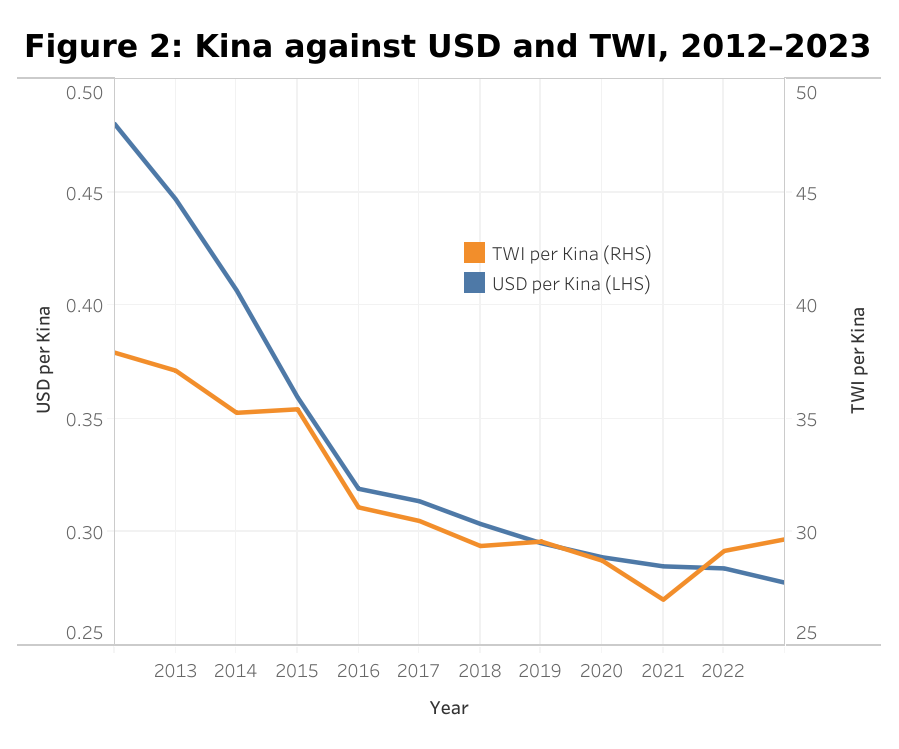

The next graph takes a longer-term view. Since 2012, the kina has depreciated twice as much against the US dollar as against the TWI (42 per cent vs 22 per cent).

Notes: Exchange rate values are for the last day of each month.

Why TWI matters

Greater focus on the TWI is justified for several reasons. First, when the kina is depreciating against the USD, we need to know whether this is part of a general global trend of USD strengthening or a PNG-specific outcome.

Second, depreciation leads to inflation, but this will be better captured by the TWI rather than the USD-kina exchange rate. For example, imports from Australia are likely to be invoiced in Australian not US dollars.

Third, depreciation will help reduce demand for imports and thus foreign exchange rationing, but only if it is relative to the currencies in which goods are priced. Again, this makes the TWI much more relevant than the USD exchange rate.

Fourth, according to the IMF, BPNG will shortly be announcing an explicit “crawling peg” strategy for the kina. In the 1970s and 1980s, the kina was pegged to a trade-weighted basket of currencies rather than a single currency. (The kina was originally pegged to the Australian dollar, but in 1977 the shift was made to peg to a basket of currencies.) This could once again be an appropriate policy.

More data, please

Given its importance, it is not good enough for BPNG to release its TWI data with a lag of half a year or more. BPNG could easily publish the TWI every month, or even every day. In the meantime, we have to rely on our estimates which show that, for all the talk about it, on a trade-weighted basis there was actually only very modest depreciation last year. Underlying data available here.

Disclosure: This research was undertaken with the support of the ANU-UPNG Partnership, an initiative of the PNG-Australia Partnership, funded by the Department of Foreign Affairs and Trade. The views are those of the authors only.

This article appeared first on Devpolicy Blog (devpolicy.org), from the Development Policy Centre at The Australian National University.

Bobby Kunda is an economics lecturer at the University of Papua New Guinea. Stephen Howes is Director of the Development Policy Centre and Professor of Economics at the Crawford School of Public Policy at The Australian National University.