The 2022 PNG 100 CEO Survey: the return of optimism

The PNG 100 CEO Survey captured the depth of the COVID crisis through 2021, and is now charting a return of some optimism in 2022, according to analysis provided by Westpac’s Senior Economist, Justin Smirk.

After 11 years of data, we are now seeing some trends regarding business impediments in PNG: where improvements have been made, where there has been slippage and where there is more work to be done.

The number one message from the survey is that COVID remains one of the most significant shocks to hit PNG businesses since the start of the survey and we are still a long way from getting out of the woods, even though some other issues are now more pressing.

Westpac’s Justin Smirk

Without the support of a significant resources project, PNG’s business leaders are telling us that the country’s economy remains vulnerable to any external shocks (including further COVID impacts and the Russia–Ukraine war) and the expected recovery is modest and gradual, compared to the V shaped recovery being experienced by many other nations.

From the 2022 survey, we have identified four key highlights:

1. Profits in 2021 were better than anticipated and are expected to be better in 2022

But they’re still below average. Last year, we were disappointed that profit expectations for 2021 were not greater. Given the magnitude of COVID-19’s hit to profits in 2020, we were surprised businesses were not expecting a stronger bounce.

‘This year’s results suggested PNG businesses are maintaining a degree of caution.’

In this year’s survey, however, profit results for 2021 exceeded business leaders’ expectations by a margin not seen since 2012. This outperformance is a very promising result.

Some 25 per cent of firms reported that their profits greatly exceeded expectations – much higher that the 10 per cent in 2021 and the highest since 30 per cent in 2013. Meanwhile, 33 per cent reported profits slightly exceed expectations, 25 per cent said profits had met expectations, while 17 per cent reported profits slightly short of expectation. No one reported profits substantially short of expectations – the last time this was the case was in 2019.

Through the history of the survey, we are yet to see a year when our CEOs were not expecting better profits this year than last. Given this natural optimism, we should therefore ask: is the expectation of a lift in profits greater, or less, than usual?

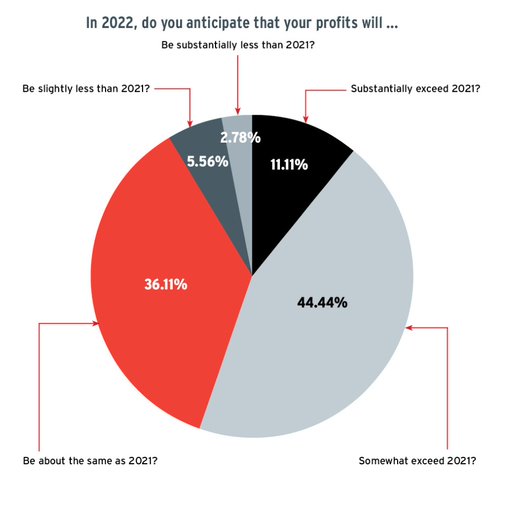

This year’s results suggested PNG businesses are maintaining a degree of caution. Only 11 per cent expected profits to be substantially higher than the previous year (compared to 18 per cent in 2021), 44 per cent expected them to somewhat exceed the previous year (compared to 28 per cent in 2021), while 36 per cent expected profits to be the same (compared to 38 per cent in 2021).

‘While the expectations for profits and investment have lifted they are still well down on the results of the 2019 survey.’

The number of businesses expecting profits to be less than the previous year fell from 9.0 per cent in 2021 to 4.0 per cent this year.

2. Recruitment, investment and profit expectations lifted in 2022 but are still to fully recover

The survey asked CEOs for their recruitment, investment, and profit expectations for 2022. Combining these three, we have created a weighted net balance of the sum of their expectations: a Business Confidence Index, if you will. This index improved in 2022, lifting from 66.3 in 2021 to 78.0, the strongest level since 2019 (93.3).

While the expectations for profits and investment have lifted they are still well down on the results of the 2019 survey.

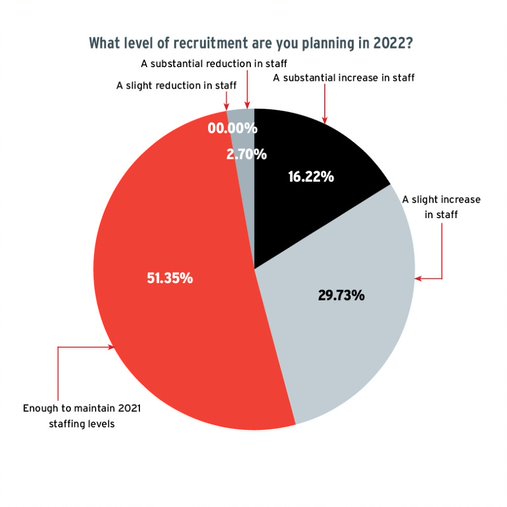

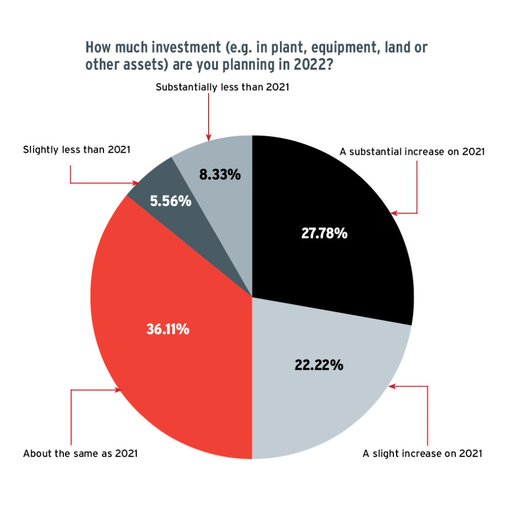

The Profit Expectation Index lifted to 55.5 from 37.4 but it is still meaningfully lower than the 90.0 in 2019. The Investment Expectation Index lifted to 55.6 from 40.0, although this is less than half of the 113.3 index in 2019. Meanwhile, the Employment Expectation Index is up from 20.0 in 2021 to 56.8, which is higher than the 56.6 of 2019. This is a promising sign for stronger growth in formal employment.

Over its 11 years, the PNG 100 CEO Survey has consistently reported that employment is expected to grow while the official data has been more volatile, which suggests an upward bias on employment expectations.

Thus, the 56.8 result for 2022 should be considered relative to the survey’s 11-year survey average of 40.6. This makes it easier to compare the survey to PNG’s official nonminerals employment, which saw something of a recovery through 2019 and only a modest correction through 2020 and 2021.

The current survey is pointing to a possible solid recovery in employment through 2022 (although a lot will depend on the public sector employment for the final official figure).

3. A modest lift in expectations points to a modest lift in growth

There seems to be a broad expectation from forecasters for the PNG economy to grow 4.0 per cent this year, building on the modest 1.0 per cent recovery in 2021.

While there was a recovery in employment, most likely related to the opening of the economy from the COVID restrictions, businesses remain uncertain on profits and investment. Without a positive boost of a large of resources project this year, the PNG economy remains vulnerable, suggesting downside risks to the 4.0 per cent forecast.

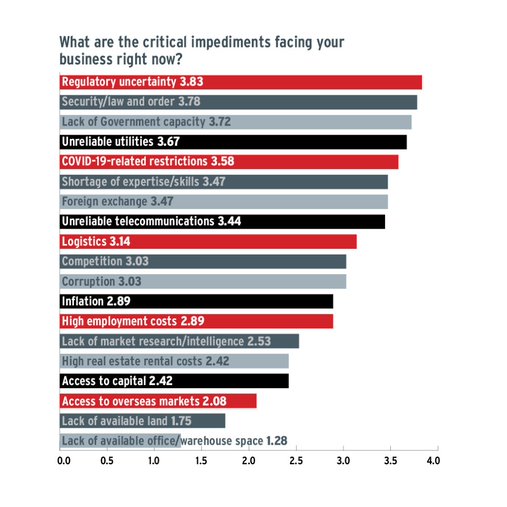

4. Security, law and order now a bigger constraint on business than COVID restrictions

The PNG 100 CEO Survey asks CEOs about the top constraints on their businesses. Since 2014, the top five have been: foreign exchange (FX), security/law & order, unreliable telecommunications, unreliable utilities and lack of government capacity.

From 2016 to 2019, as liquidity improved, FX dropped back down the list but in 2020 it popped back to be the most significant constraint and it was only beaten in 2021 by COVID restrictions.

This year, FX has dropped back to being of the same level of concern as unreliable telecommunications.

Telecommunications have been improving since the 2019 survey and are now a much less significant constraint than they were. There have been similar improvements in utilities and skill shortages over time, but unreliable utilities lifted as a concern in 2022.

Of concern is that we come out of the COVID restrictions with three key foundations of any economy – law and order, government capacity and regulatory uncertainty – found to be wanting. The lack of government capacity was very telling in 2021 with the additional stress of the COVID outbreak but in 2022 it is again the third most significant constraint behind regulation and security/law and order. Rising regulation concerns is an issue if it provides a brake on potential investment. Security/law and order have been a consistent issue in this survey and given the social and economic disruptions in 2021 it is good to see there was not a greater lift in business concerns this year.

Rising regulation concerns is an issue if it provides a brake on potential investment. Security/law and order have been a consistent issue in this survey and given the social and economic disruptions in 2021 it is good to see there was not a greater lift in business concerns this year.

COVID restrictions have dropped to the fourth most significant concern. There has been a recent deterioration in logistic services compared to the improving trend seen from 2016 to 2020. A large part of this would be the disruptions to global distribution networks, which should start to improve in late 2022. This is nevertheless a key point of concern.

Finally, while still relatively low compared to other times in the survey’s history, rising concerns about inflation are not surprising given emerging global inflation concerns. This is something the Bank of PNG will be watching closely, given it presents a significant risk to the economy. High employment costs remain a concern but not more so than they have been for a number of years.

Justin Smirk is Senior Economist at Westpac.

The 2022 PNG 100 CEO Survey was conducted between November 2021 and January 2022. The survey polled senior executives from a representative sample of PNG’s largest companies, across all sectors of the economy. To download the full report of this year’s survey, click here.