2021 PNG 100 CEO Survey: a snapshot of the effects of COVID-19 in Papua New Guinea [analysis]

The annual Business Advantage/Westpac PNG 100 CEO Survey has captured the depth of the COVID-19 crisis and the sense of uncertainty that exists among businesses in Papua New Guinea. Westpac’s Senior Economist Justin Smirk takes a closer look.

Click on the above image to download a copy of the 2021 PNG 100 CEO Survey.

In the ten years of data collected by the PNG 100 CEO Survey, some trends are emerging. We can see where improvements have been made to business conditions in PNG, where there has been slippage, and where there is more work to be done.

However, the number one message from this year’s survey is that COVID-19-related restrictions were, and remain, the most significant shock to hit PNG businesses – and everyone is still a long way from getting out of the woods.

Without the support of a significant resources project, the PNG economy remains vulnerable to any external shocks (including further COVID-19 restrictions) and the recovery expected is modest and gradual compared to the V-shaped recovery being experienced by many other nations.

Here are the four trends we identified from the 2020 survey.

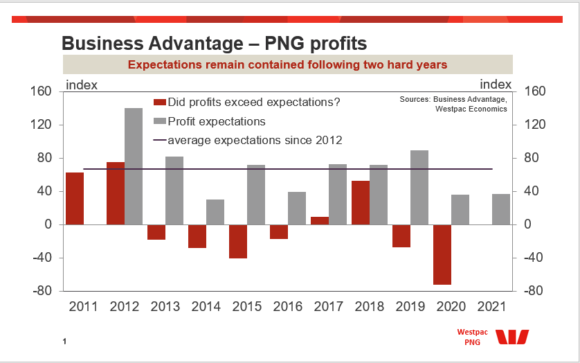

1. COVID-19 hit profits and the expected rebound is very disappointing

The global pandemic has been the biggest shock to PNG business profits in the short life of the survey. Only 13 per cent of firms reported that 2020 profits exceeded expectations, 28 per cent said they met expectations, 59 per cent reported profits falling short of expectations, and 35 per cent reported a substantial fall below expectations (the previous highest share for a substantial fall below expectations was 18 per cent in 2014).

What is disappointing is the lack of a significant bounce in the expectation for profits in 2021. Throughout the history of the survey, firms have expected an improvement in profit in the current year compared to the previous year.

‘Expectations remain below the historical averages, suggesting a below average outcome for employment, investment and profits.’

The lift in expectations varied from year to year, but there has never been be a year where profit expectations for the current year were not positive.

An expected rise in profits is a base or neutral position. Given the size of the COVID hit to profits in 2020, which followed a disappointing profit outcome in 2019, you would hope that the expectations for profits in 2021 would be larger than usual.

This is not the case, with a weighted 37.5 per cent reporting lift in expectations for 2021, only marginally higher than the 36.6 per cent reported in 2020 and well below the average for the survey history of 67.5 per cent. Following two disappointing years, firms appear to be resigned that 2021 is going to be another disappointing year.

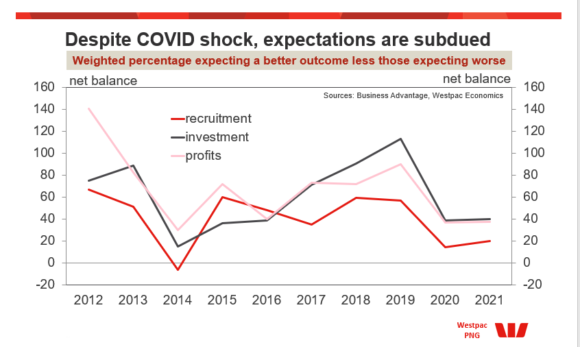

2. Recruitment, investment and profit expectations went sideways for 2021

Expectations remain below the historical averages, suggesting a below average outcome for employment, investment and profits.

While plans for investment and recruitment were more upbeat than 2014’s low, profits remain just on par. Given the magnitude of the COVID-19 shock, it is very disappointing that businesses are not looking for a more meaningful recovery.

This is very worrying for formal employment expectations. In each year of the survey, employment has been expected to grow but the official data has been more volatile than that. The 20 per cent result for 2021 should be considered relative to the average of 37.7 per cent. For investment expectations, the print was 40.0 per cent, compared to an average of 59.2 per cent, while profits printed 37.7 per cent compared to the historical average of 59.3 per cent.

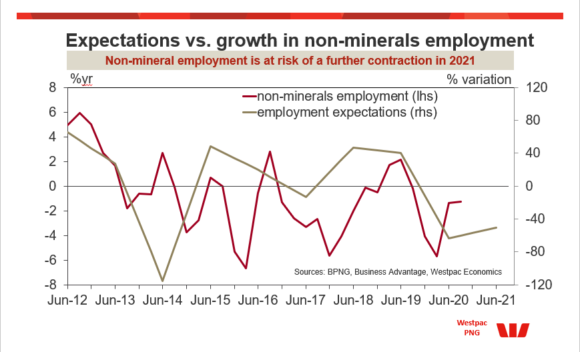

For employment in particular, the outlook is not very promising. So far, the hit to formal employment from COVID-19 has been relatively modest given that it is on par with the last downturn through 2017 and 2018. However, the poor employment expectations for 2021 suggest that it is likely formal employment in the nonminerals sector will contract again through 2021. We are still some distance away from a robust sustainable recovery in employment.

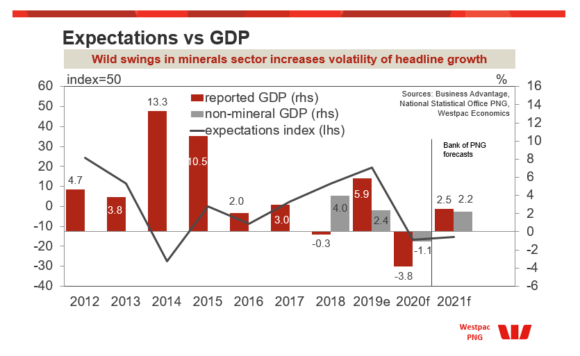

3. Flat expectations raise questions on how robust the recovery will be

In the March Monetary Policy Statement, the Bank of Papua New Guinea (BPNG) forecast the economy to grow 2.5 per cent in 2021 following a -3.8 per cent contraction in 2020. COVID-19 shock hit the economy hard, but we can see that there is more going on than just the pandemic.

While total GDP rose 5.9 per cent in 2019, fell -3.8 per cent in 2020 and is forecast to rise 2.5 per cent in 2021, non-mineral GDP rose a more modest 2.4 per cent in 2019, fell a smaller minus 1.1 per cent in 2020, while the BPNG is forecasting a bounce of 2.2 per cent in 2021.

The completion of large resources projects and the delay or cancellation of new projects had a bigger impact on overall economic growth than the COVID-19 restrictions did in 2020. With COVID restrictions behind most of the contraction in non-mineral economic activity in 2020, the reopening of the economy in 2021 should see a bounce.

As such, the outlook is tied to how quickly the pandemic is brought under control. Businesses remain very uncertain and, without a positive external shock of a large of resources project, the PNG economy remains vulnerable to new outbreaks.

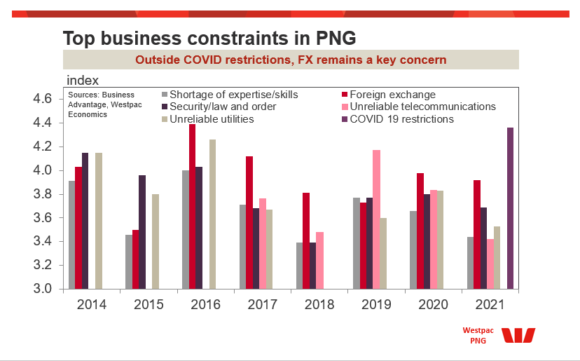

4. Outside of COVID-19, foreign exchange remains the business constraint

Since 2021, the top five constrains identified have been: skill shortages, foreign exchange (FX) availability, security, unreliable telecommunications, and unreliable utilities.

From 2016 to 2019, as liquidity improved, FX dropped back down the list but in 2020 it popped back to be the most significant constraint and it was only beaten in 2021 by COVID-19 restrictions.

Telecommunications improved from 2019 and are now seen as a much less significant constraint than they were.

There have been similar improvements in utilities and skills but there has been little change in law and order.

It is tempting to see the effect of COVID-19 restrictions swamping other issues but the fact there was no real improvement in FX or security/law and order suggests these issues are significant in their own right. It is also interesting to note the jump in logistics being a constraint on businesses in 2021 compared to the improving trend seen since 2016. COVID restrictions have significantly disrupted transport and distribution networks and you would expect that this to improve as the restrictions are lifted.

Justin Smirk is Senior Economist at Westpac.

The 2021 PNG 100 CEO Survey was conducted by Business Advantage International between January and March 2021. The survey included senior executives from a representative sample of PNG’s largest companies, across all sectors of the economy. To request a free copy of the full survey results, click here.