Analysis: How the Papua LNG project should improve PNG’s financial imbalances

The go-ahead for the US$10 billion Papua LNG project is likely to do much to alleviate some of the financial imbalances in the PNG economy, including the lack of availability of foreign exchange and the weakness of the currency. David James investigates.

The ExxonMobil-led US$19 billion PNG LNG project, which started exporting gas in 2014, has proved to be a success, leading to a surge in PNG’s exports.

But it also resulted in an anomalous situation whereby PNG enjoys a large trade surplus, but has a large and growing deficit on its capital and finance account. Despite the country doing well on the trade front, money has been flowing out of PNG, much of it to pay interest on the debt used to fund the PNG LNG project.

Thus the Bank of Papua New Guinea’s December 2018 Quarterly Economic Bulletin attributed the financial imbalance to a ‘build-up in offshore foreign currency account balances of mining, oil and LNG companies.’

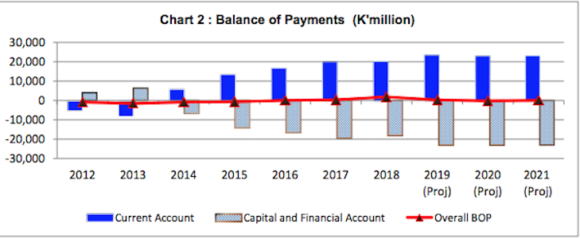

PNG’s capital and finance account deficit is predicted to continue worsening until at least until 2021, as this chart from the central bank’s March Monetary Policy Statement indicates:

PNG’s deficit on the capital and finance account is predicted to worsen Source: Bank of PNG

What meant for business

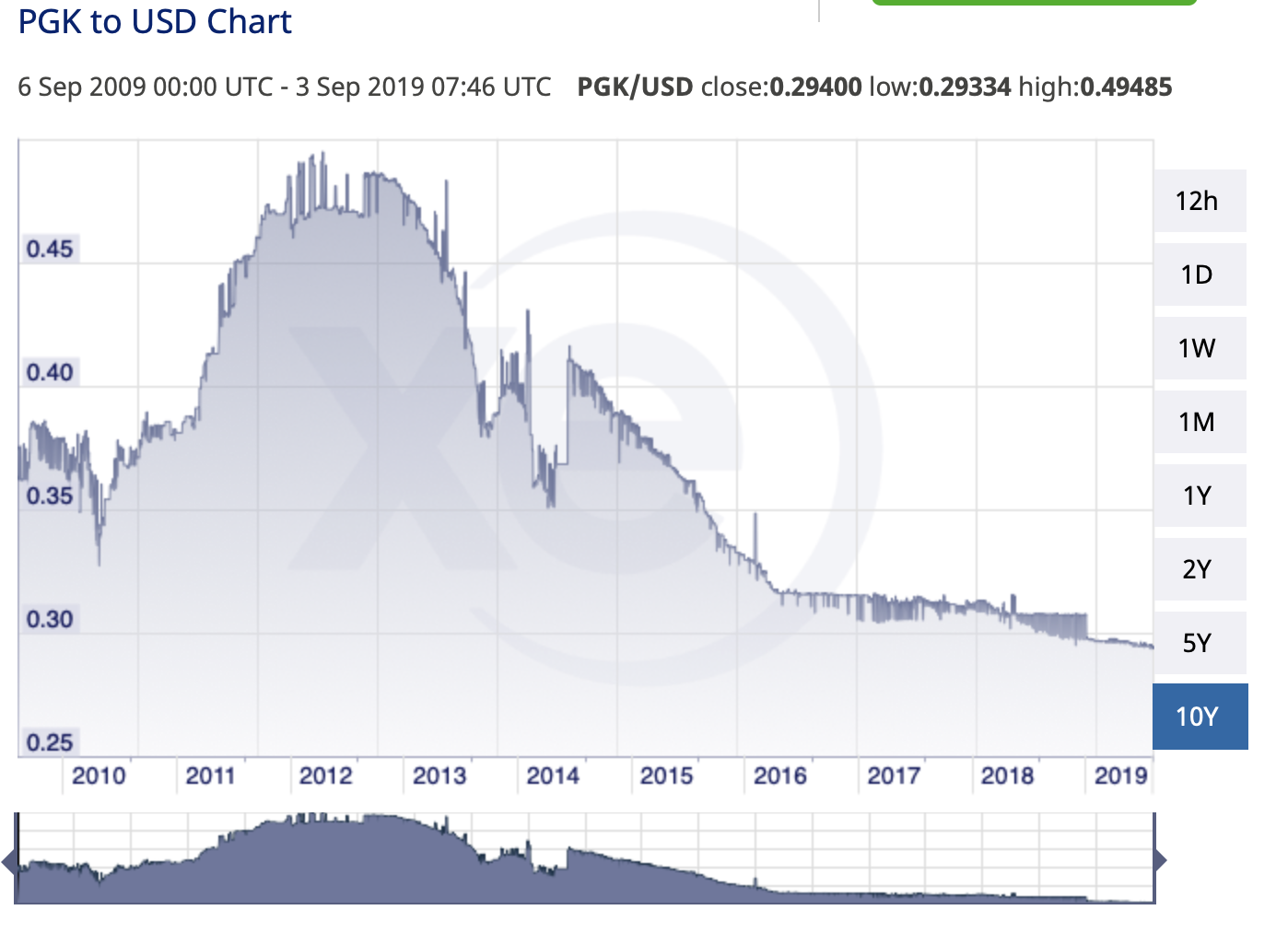

The large financial outflows have resulted in a relative lack of demand for kina-denominated assets. This resulted in foreign exchange shortages and led to a steady fall in the value of the kina, as you can see from the graph below, which shows the falling value of the kina against the US dollar since it peaked in 2011.

The Kina’s fall: a 10-year view against the US dollar Credit: XE.com

Cycles

With the Papua LNG project starting up, however, a new cycle of investment in PNG will commence, counteracting the adverse effects of PNG’s first LNG project.

‘In effect, the two cycles of LNG investment will be unsynchronized, so they will counteract each other.’

To see why, we need to go back to 2009, when the Final Investment Decision (FID) for the PNG LNG project was announced.

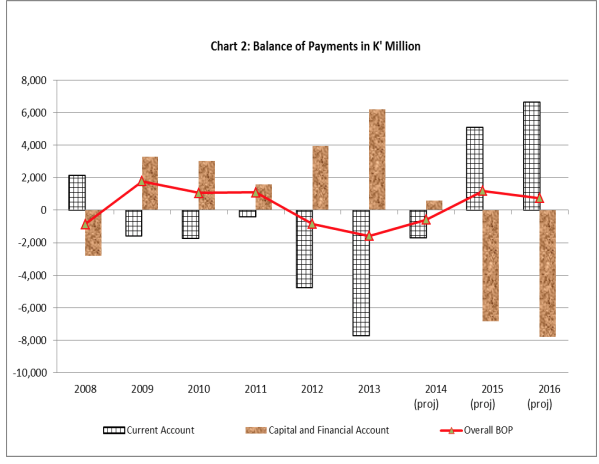

Between 2009 and 2014—the PNG LNG construction phase—PNG’s capital and financial account went into surplus. Money was coming into the country. Once the project was built and PNG LNG began producing gas, however, the project partners started paying down the debt incurred to finance the project. PNG’s financial and capital account (in brown in the chart below) went into sharp deficit.

The construction phase of PNG LNG resulted in a large surplus on the capital and finance account (in brown above). Source: Bank of PNG

If the Papua LNG project follows the same pattern, then from 2020 (the point at which the FID is expected and construction begins), there will again be significant capital inflows into PNG, counteracting the effect of the PNG LNG outflows.

In effect, the two cycles of LNG investment will be unsynchronized, so they will counteract each other.

And after construction?

Once the Papua LNG construction phase comes to an end, in the mid-2020s, there will again be heavy outflows to pay for the debt incurred.

But at that point, the LNG PNG debt will have been paid off and there will be significant revenues flowing to the government.

Gerea Aopi, President of PNG Chamber of Mines and Petroleum, says that there will be large benefits to the government.

‘In the mid-2020s, once all the debt is paid off, there will be a new problem in terms of a lot of revenues going to the state.’

It will mean that PNG’s comparatively small economy, which has been disproportionately affected by the sheer size of the PNG LNG project, will get some much needed protection from another large project commencing.

When the revenues from PNG LNG start coming into the government, they can also form the basis of the long-expected Sovereign Wealth Fund, which would further protect the economy.