Why is Bank South Pacific looking to list on the Australian Securities Exchange?

Bank South Pacific, Papua New Guinea’s biggest bank, has announced that it will seek secondary listing on the Australian Securities Exchange. David James considers the reasons behind the move and the implications.

BSP’s Solomon Islands head office in Honiara

Last month, after a special meeting of shareholders, BSP announced that its directors would be able to make the rules and policies for its share register that would apply in Australia as well as PNG.

‘The company will now progress with its proposed secondary listing of its ordinary shares on the Australian Securities Exchange (the ASX),’ it said in a statement.

As well as the change of rules and policies, its company name will be changed to BSP Financial Group Limited.

So, why is the bank, which has businesses in PNG, Fiji, Solomon Islands, Vanuatu, Samoa, Tonga and the Cook Islands but none in Australia, listing there?

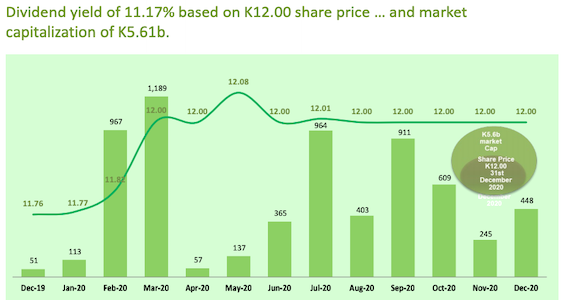

BSP share price 2019-20 (line) and trading volumes (bars). Source: BSP

Liquidity

If BSP can list on the ASX, it would make itself a target not just for Australian investors but investors from other countries who invest in the ASX.

This would improve the ease with which investors can buy or sell BSP shares (liquidity), which potentially makes the company more attractive to investors who want to be able to trade in its shares whenever they wish.

Lars Mortensen, Managing Director of stockbroker JMP Securities, says that a secondary listing would give BSP access to a deeper pool of investors.

‘They will no longer be relying exclusively on kina sources of capital. There is a chance they could access the international capital markets for fresh funding at some point in the future. It starts with equity (shares), but it may in time involve other sorts of finance that involve debt instruments or hybrids. It is positive in that respect,’ he tells Business Advantage PNG.

Diversification

A dual listing for BSP may also provide PNG’s institutional investors (such as the country’s superannuation funds), with more options in terms of managing their portfolios, argues Mortensen.

‘One of the features of the investment market in PNG is that most major institutions have significant exposure to BSP as part of their current portfolios.

‘The bank will be required to pay dividends in Australian dollars to investors holding the stock on the ASX.’

‘Whilst BSP continues to be a strong performer, they [institutional investors] may want to increase their levels of diversification and there hasn’t been any way to get that because BSP is such an outsized part of local markets.

‘It will also be interesting to see which institutions decide to divest some of their holdings and – just as importantly – what those PNG institutions decide to buy with the proceeds from their divestment.’

Pressures

The move is not without its challenges. A dual listing will introduce some foreign currency liquidity and exchange rate pressures on BSP. The bank will be required to pay dividends in Australian dollars to investors holding the stock on the ASX.

‘These foreign currency-denominated dividends will need to be sourced and funded from BSP’s operations. That is a challenge, but they are a big company with unique access to, and visibility in, foreign exchange markets. They have a pathway to pay those dividends, unlike a lot of other businesses,’ notes Mortensen.

‘Fundamentally, the profit they make will be determined by how they trade in PNG, so it will still be overwhelmingly kina-sourced.’

Exchange rate movements between the kina and the Australian dollar will also affect BSP’s share price.

‘The currency risk, I guess, comes from the fact that the exchange rate movements will automatically translate into the share price. The underlying value will be in kina, which will be converted into Australian dollars for the Australian market.’

How does BSP measure up?

BSP Haus in Konedobu, Port Moresby

How does BSP compare with Australian banks and what will make its shares attractive to ASX investors?

The way bank shares are valued in Australian and global markets needs to be considered in the context of the dual listing of BSP, says Lars Mortensen, General Manager of JMP Securities.

In PNG, he notes, the focus of investors is typically on a share’s dividend yield, and price of that share divided by what it earns per share (the price–earnings ratio, or multiple of earnings).

In the Australian market, however, the price-to-book ratio (which compares the share price relative to the company’s net assets) is also considered important when valuing bank stocks.

‘Whilst BSP has a very attractive dividend and earnings yield, on a price-to-book basis BSP is not very cheap when compared to Australian banks,’ he says.

‘That is the one metric where they are a little bit more fully priced in the Australian context. They have a high dividend yield and their multiple of earnings is not outrageous. Arguably, the higher price-to-book ratio is reflective of the higher returns on equity achieved by BSP than some comparators.’

Another area where BSP differs is the amount of capital it retains, known as the capital adequacy ratio.

Most Australian banks retain about eight per cent of their capital, but BSP has a 23.3 per cent capital adequacy ratio, making it an extremely conservatively-managed bank.

‘The reality is that it is very well capitalised by any international standards,’ says Mortensen. He notes that the ‘flip side’ is that investors in international markets are likely to consider there to be a high country risk in PNG.