Bank South Pacific continues to dominate but faces risks, say analysts

Bank South Pacific, Papua New Guinea’s biggest bank, has made ts 2017 AGM shareholder presentation. Analysts say it indicates the bank is travelling strongly, but does face some risks.

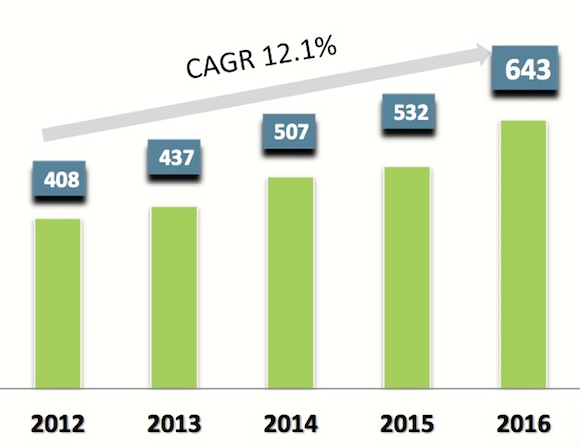

BSP’s net profit after tax (in million kina). Source: BSP

According to the bank’s shareholder presentati0n, net profit after tax (NPAT) was up 21 per cent to K643 million. Total income was up 16 per cent to K1.79 billion, while total costs rose by 11.4 per cent. In PNG, the bank has a 55 per cent market share in loans, and a 57 per cent market share in deposits.

Capital adequacy (the amount of capital retained for risk mitigation) was 23.1 per cent, almost double the global requirement. Return on equity was similarly high by global standards. It rose by 1.8 per cent to 29.6 per cent.

Dominant

According to Oliver Ryan and Junior Gotaha, analysts with Pacwealth Capital, the bank continues to be the market leader. ‘BSP remains the dominant player by customers, assets, profits and Return on Equity.’

‘Exposure to commercial and corporate loans is a key risk.’

Ryan and Gotaha describe the full-year dividend as impressive. ‘One hundred and four toea translates to a yield ‘in excess’ of 10 per cent. That is impressive considering BSP shares have increased by over 25 per cent over the past 12 months.

‘Compare this to the Bank of PNG 364-day Treasury Bills, which are yielding about 7.8 per cent.’

Risks

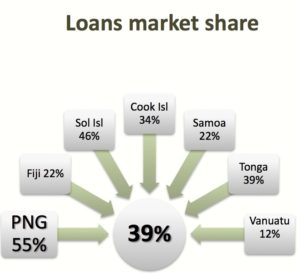

BSP’s loan market share in its various countries of operation. Source: BSP

Oliver and Gotaha say that 66.4 per cent of the bank’s total loan portfolio is within PNG, which potentially brings dangers.

‘As evidenced in S&P’s April rating review, BSP’s exposure to commercial and corporate loans is a key risk—a risk exposure which grew 17.2 per cent across the group in 2016 to K10.1 billion. There was a further K320 million in the first quarter of 2017 alone, a 3 per cent increase on the previous quarter.

‘Delayed loan payments due to the PNG election cycle, the sluggish domestic economy and foreign currency shortages are likely to result in credit pressures, which may force write-downs.

‘Thus, 5 per cent provisions-to-loans (provisions for bad debts) appears unobjectionable, albeit high by global banking standards.

‘Over the long-term, given that loan penetration across the Pacific is low, BSP is best positioned to capitalise on this opportunity and diversify its loan book.’

Strategy

Oliver and Gotaha believe the bank’s strategy is likely to be a continuation of its existing approach.

‘BSP will make little change to its strategy. It will continue to gain deposit customers from under-banked regions, churn out loans and look to gobble up asset finance businesses.

‘A Joint Venture with RMA Finance Cambodia PLC was finalised in early May.’

‘Eighty per cent of the PNG population is unbanked, with PNG loan penetration at only 28 per cent—significantly below that of developed markets and many other emerging markets. Furthermore, only 9.4 per cent of the population has access to mobile banking.’

Not all the strategies are business as usual, however. A Joint Venture with RMA Finance Cambodia PLC was finalised in early May. It will be rebranded BSP Finance (Cambodia) PLC.

Liquidity

BSP’s share price history Source: BSP

Plans to dual list seem to be on hold. Any dual listing in Singapore has been shelved because the ‘process became prolonged and outside the desired project timeline’.

Regarding of any ‘potential’ listing on the Australian Securities Exchange, the bank indicated that there would not be a significant offer of shares if it eventuates.

An advantage of dual listing is that it would increase liquidity (trading volume). Oliver and Gotaha identify this as a potential area of weakness.

A lack of new strategic directions may bring risks. ‘Interestingly, the conclusion slide from the BSP AGM in 2016 was exactly the same as the 2017 meeting,’ comment Oliver and Gotaha.

‘Will investors be happy to see the same conclusions at the 2018 AGM, without any improvement in shareholder liquidity?’