Commodity cycle turning up, says ANZ economist

The long commodity bear market is coming to an end, according to Richard Yetsenga, Chief Economist for the ANZ Banking Group. He also observes that, in a world growing more sceptical about globalisation, there is growing competition for foreign direct investment.

The ANZ’s Richard Yetsenga Source: ANZ

‘The commodity bear market which began in 2008, and again from 2011, I think finished in early 2016. Since then, we have been in this quasi-‘twilight zone’ of modest ranging de-correlated commodity price movements,’ Yetsenga commented at a recent industry event in Port Moresby, Papua New Guinea.

‘I think now, however, for the first time since pre-crisis a number of elements are falling into place that suggest a more concrete commodity bull market.

‘Demand is broader and more enduring than at any stage since the financial crisis.

‘Supply adjustments remain meaningful. Structural change in the US shale industry and structural reform in China I think are all meaningful contributors to only modest supply growth.

‘These forces are being augmented by newer sources of demand such as electric vehicles and renewables and I think this is resulting in higher demand for commodity product.’

Slow burn

Yetsenga added that ‘behind the scenes’ there are some ‘slower burn issues’ that point to stronger commodity prices.

‘China also has become focused on the quality of growth.’

One of these is the push to build more infrastructure across the Asian region.

‘In China, there are trade and strategic ambitions through the One Belt One Road initiative.

‘China also has become focused on the quality of growth and is acting to remove capacity which doesn’t fit with that aspiration.’

Soft commodities

Yetsenga said PNG’s dependence on commodity exports ‘looked to be a challenge in recent years’ but is now ‘looking to be more of a strength’.

But he detects a ‘noticeable’ imbalance in favour of hard commodities.

‘Soft commodity production tends to be more fragmented.’

‘The level of soft commodity exports (commodities grown rather than mined) is only around 10 per cent of the hard commodity sector. Hard commodity exports are dominated by large producers supported by technology, capital and know-how.

‘Soft commodity production tends to be more fragmented and smaller scale. So it relies more on government-provided infrastructure.’

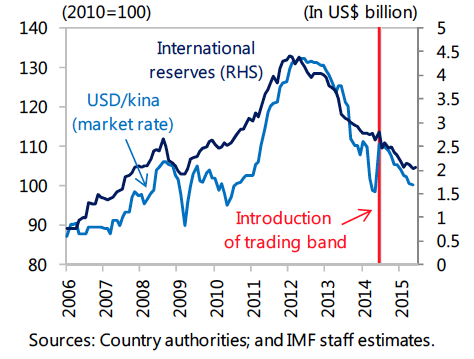

Exchange rate

PNG’s exchange rate and reserves (against US$) Source: IMF

Yetsenga said to get the correct policy on PNG’s exchange rate requires understanding the specifics of the economy.

‘The key question is what arms of policy will be willingly be subordinated to the exchange rate?

‘An economy that is commodity-centric, [which] has a highly flexible exchange rate, can be prone to more issues of Dutch disease.’

‘I don’t accept that having an open capital account and flexible currency, perhaps of the sort seen in Australia and New Zealand, is the default best option for every country at every stage of development.

‘An economy that is commodity-centric, [which] has a highly flexible exchange rate, can be prone to more issues of Dutch disease or large resource transfers between the commodity and non-commodity sectors.

‘For an economy where the terms of trade does show wide and sustained cycles, the exchange rate is almost certainly an important part of the adjustment mechanism to those cycles.

‘At the other end of the spectrum is a currency peg or fixed exchange rate—for instance China since 2005.

‘This may be appropriate for short periods. The reality, however, is that countries that have successfully run a fixed exchange rate, or tightly managed exchange, for extended periods are few and far between.’

Foreign Direct Investment

ANZ econmist Richard Yetsenga said many countries are ‘laying out the welcome mat’ to attract foreign direct investment (FDI).

‘In this more sceptical phase of globalisation global competition for foreign direct investment if anything has become more intense.

‘Competition in corporate tax rates has become particularly focused.

‘There is a constructive regional dynamic around FDI but it is selective. It is only really growing in a handful of countries in the region: China, Hong Kong, Singapore and India. Elsewhere, foreign direct investment has not had a cyclical recovery.

‘FDI in PNG has become more sporadic and is significantly influenced by the particular projects.’

Inflation

Yetsenga expressed concern about recent rising inflation. ‘Economies with an inflation premium almost always have an infrastructure deficiency.

‘This in turn reduces the flexibility of the economy and makes it more inflation prone. Structural gains should be strongly protected.’