Debt crisis looming: reports say Papua New Guinea needs new investment

Papua New Guinea is facing a debt crisis according to new reports from the Asian Development Bank and the World Bank, and the country will need the cash injection of new major investments to avoid ‘lacklustre’ future growth.

The Central Bank has announced it will buy back some government debt, a practice known as ‘quantitative easing’. Source: BAI

Two new reports show that the twin shocks of the COVID-19 virus and a sharp drop in oil and gas prices will see PNG heading for debt crisis unless new oil and gas projects can offer a financial lifeline.

A report by the Asian Development Bank (ADB), Asian Development Outlook 2020, says that the PNG government is likely to go further into debt. ‘As the fiscal balance worsens, the government faces important challenges in managing public debt, including arrears, contingent liabilities, and state-owned enterprise debt,’ the report says.

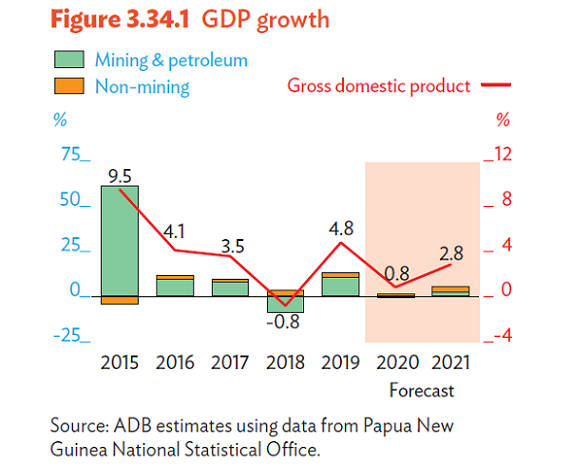

‘In the absence of major new investments in extractive industry commencing in the short term, growth will remain lacklustre.’

The ADB report forecasts GDP growth of 0.8 per cent this year and 2.8 per cent next year. Inflation is expected to be 3.3 per cent this year and 4.4 per cent in 2021.

‘In the absence of major new investments in extractive industry commencing in the short term, growth will remain lacklustre,’ the report says. ‘Gas production is expected to plateau but could fall in 2020 in response to reduced demand from the People’s Republic of China (PRC) because of COVID-19. PNG sells about a quarter of its gas to the PRC, mostly on long-term contracts.’

The ADB report says gold and copper production is expected to expand, with the entire world looking to the safety of the gold standard at a time of uncertainty, although there could be setbacks with COVID-19, affecting supply chains and staff movement to and from mine sites. ‘The Ok Tedi gold and copper mine and the Lihir gold mine are both expected to increase production in 2020 and 2021 thanks to recent and ongoing capital investment.’

Managing the debt

The ADB report outlines three areas where the debt problems for the government will need to be managed:

The ADB report outlines three areas where the debt problems for the government will need to be managed:

- ‘Large amounts’ of public sector arrears in the form of unpaid bills, mainly wages, allowances, and unpaid invoices for its purchase of goods and services.

- State-owned enterprises debt, which ‘neither the Treasury nor any other department is actively monitoring’.

- Contingent liabilities, which were estimated in 2019 to be K14.1 billion, 91 per cent of which are guarantees extended to external creditors. ‘In the past, the servicing of both principal and interest costs of some guaranteed loans has become a burden on the government budget.’

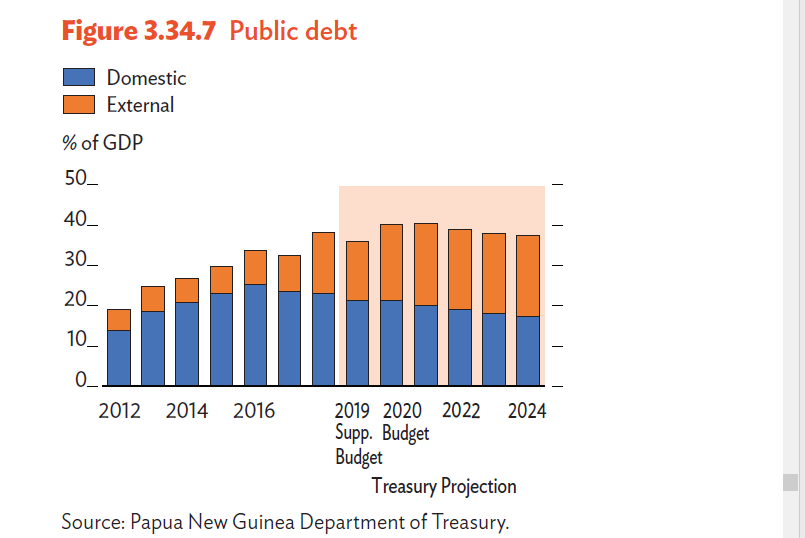

The report adds that central government debt at the end of 2019 stood at K32.5 billion, equal to 38.1 per cent of GDP. This was up from K29.7 billion, or 36.2 per cent of GDP at the end of 2018.

World Bank looks to LNG

The World Bank report, East Asia and the Pacific in the time of COVID-19, points to a possible glut in the LNG market because of a slow-down in China. It says this is being exacerbated by a new oil price war because of ‘plummeting oil and LNG prices’.

The World Bank report, East Asia and the Pacific in the time of COVID-19, points to a possible glut in the LNG market because of a slow-down in China. It says this is being exacerbated by a new oil price war because of ‘plummeting oil and LNG prices’.

The report also says this will create problems in managing government debt levels. ‘These developments will lead to negative implications for resource revenue flowing to the external and fiscal accounts of PNG.

‘Although external risks are out of the government’s control, the authorities should continue working on improving the economic and fiscal resilience of Papua New Guinea’s economy.’

‘The BPNG now has the option to step into the market and buy securities and prevent a blow out in interest rates.’

The Bank of PNG (BPNG) has announced it will buy back government debt, a practice known as ‘quantitative easing’.

Justin Smirk, a Senior Economist with Westpac Bank, comments that when the bank buys back the securities it reduces the government’s debt burden because ‘any interest the bank earns from holding the bonds can be returned to the government, in the form of dividends, and thus lowering the government’s net funding costs for any given level of bond issuance.’

He notes, however, that, as the government funding requirement grows with the impact of the COVID-19 shock, the supply of government securities (debt) will surge.

‘The BPNG now has the option to step into the market and buy securities and prevent a blow-out in interest rates. Just how much they will have to buy will depend on the market’s appetite for government securities and the government’s ability to access concessional multilateral funding.

‘The risk from such a program lies in how an economy might respond to [the] increased supply of kina.’