IMF report says Papua New Guinea Government taking initiative but challenges remain considerable

A report on the state of the Papua New Guinea economy by the International Monetary Fund (IMF) says the Government has taken some ‘bold steps’ in its economic management. But it contends that the challenges are considerable and would be best managed with an ‘active’ approach to macroeconomic management.

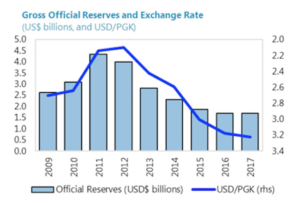

PNG’s Gross official reserves and exchange rate. Source: IMF

The annual ‘Article IV’ IMF report notes that economic activity in PNG was ‘subdued’ in 2017, leading to a slowing of money growth and credit aggregates.

Private sector credit growth is projected to have grown by 4.2 per cent in 2017, compared with 7.2 per cent in 2016. The report says the non-performing loan ratio has remained at over 3 per cent.

‘Banks, however, are well-capitalised, and continue to hold excess liquidity; another indication of weak demand for loans.’

Inflation

On a positive note, inflation is projected to decline significantly in 2017-2018, the report says, as the effects of drought dissipate and the exchange rate remains stable.

According to the IMF, the Government fiscal deficit target was 3.8 per cent of GDP in 2016; instead, it widened to 4.6 per cent.

‘In 2017, the government targeted a narrowing of the deficit to 2.5 per cent of GDP, but as of mid-year, revenue shortfalls and expenditure over-runs threatened to keep the deficit little changed from 2016.’

The combination of fiscal deficits and slow growth, the report says, has pushed the government debt-to-GDP ratio over the statutory limit of 30 per cent.

‘The capacity of the domestic financial sector to finance the deficit is over stretched, and external financing options are limited, so an important part of the budget deficit has been financed through central bank purchases of government securities and, to some extent, payments arrears. Without corrective measures, the fiscal deficit is likely to narrow slowly, pushing the debt-to-GDP.’

Financial account

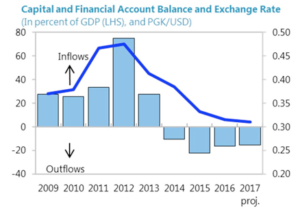

PNG’s finance account is in deficit Source: IMF

The IMF notes that the impact of the ExxonMobil-led PNG LNG project on PNG’s small economy has resulted in significant macro-economic challenges.

‘PNG’s capital and financial account balance swung from a large surplus of US$4.2 billion in 2013, reflecting inflows to finance the PNG LNG project, to a large deficit, following completion of the project, estimated at US$3 billion in 2017.

‘A large portion of this outflow has consisted of construction loan repayments.’

‘The “sustained over-valuation of the kina” should end’

The IMF report says there has also been a sharp reduction in imports, as much as half may be attributable to the reduction of imports directly associated with the PNG LNG project.

‘In addition, however, import compression, and backlogged import demand, associated with foreign exchange restrictions is likely to have played an important part.’

Passive or active?

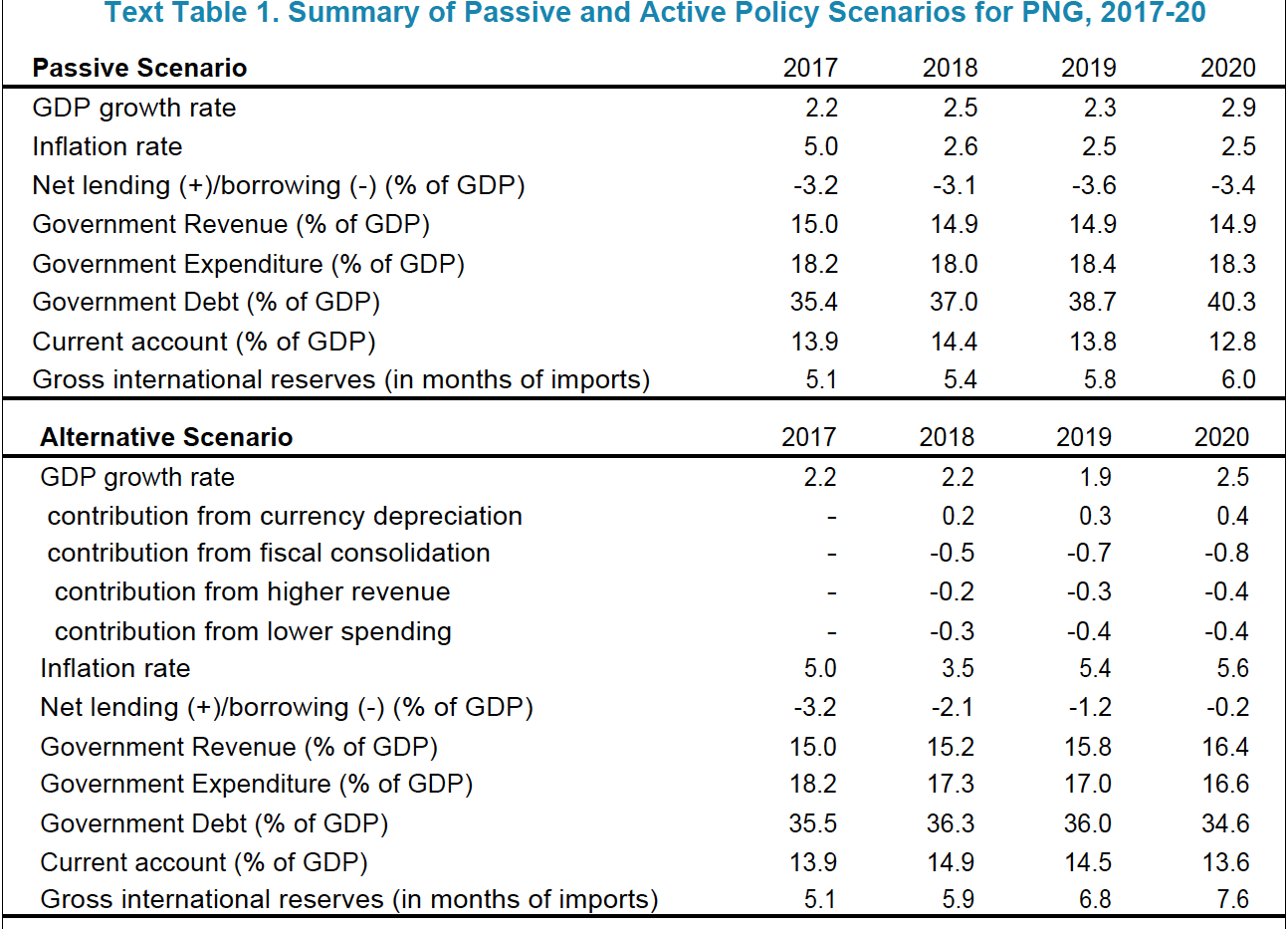

The report outlines what it calls an ‘active’ and a ‘passive’ scenario for the government in its macro-economic management (see table below). The passive scenario assumes an unchanged fiscal policy and a flat exchange rate. The active scenario assumes a declining fiscal deficit through ‘spending cuts and revenue mobilisation, together with gradual depreciation of the Kina.’

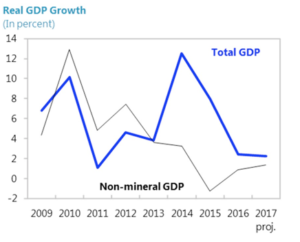

PNG’s non-mineral real GDP. Source: IMF

It says in the active scenario there is likely to be longer-term growth, especially in the non-resource sector, because of the benefits leading from the exchange rate adjustment and the completion of fiscal adjustment.

‘A high priority should be public spending on basic education, health care and infrastructure to support development of the non-resource sector’

It says in the passive scenario ongoing fiscal constraints and exchange rate overvaluation continue to dampen growth. It adds that there is a significant risk that the passive scenario will not be feasible.

‘If deficits on the scale shown in this scenario cannot be financed domestically or externally, a fiscal and financial crisis would likely ensue, leading to much worse outcomes for economic activity.

‘Conversely, in the “active” scenario there is an upside risk that a reduction of foreign exchange market distortions and fiscal consolidation could give a larger stimulus to activity through confidence effects, particularly in sectors such as agriculture.’

Strategy supported

The report says IMF staff ‘support the broad lines of the new government’s development strategy.’

It says a high priority should be public spending on basic education, health care and infrastructure to support development of the non-resource sector. But it argues that the ‘sustained over-valuation of the kina’ should end in order to end the foreign exchange shortage and promote external competitiveness.

‘Increased exchange rate flexibility is needed both to begin addressing the foreign exchange shortage and as a complement to fiscal consolidation.’

It warns, however, that a rapid depreciation would have a ‘large impact’ on inflation and ‘could be unnecessarily disruptive in the short run’.

Accordingly, a gradual approach to exchange rate adjustment and increasing flexibility is recommended.

‘Increasing the flexibility of the exchange rate should be accompanied by clarification of the monetary policy framework, measures to eliminate excess liquidity, and strengthening of the market-based operational framework.’

IMF scenarios for active and passive approach. Source: IMF staff calculations