Moody’s puts a negative rating on Papua New Guinea’s sovereign debt

The ratings agency Moody’s has affirmed Papua New Guinea’s B2 rating, but downgraded it from ‘negative from stable’, citing higher government liquidity risks, increased gross borrowing requirements and limited funding sources. It points to a growing reliance on short-term debt.

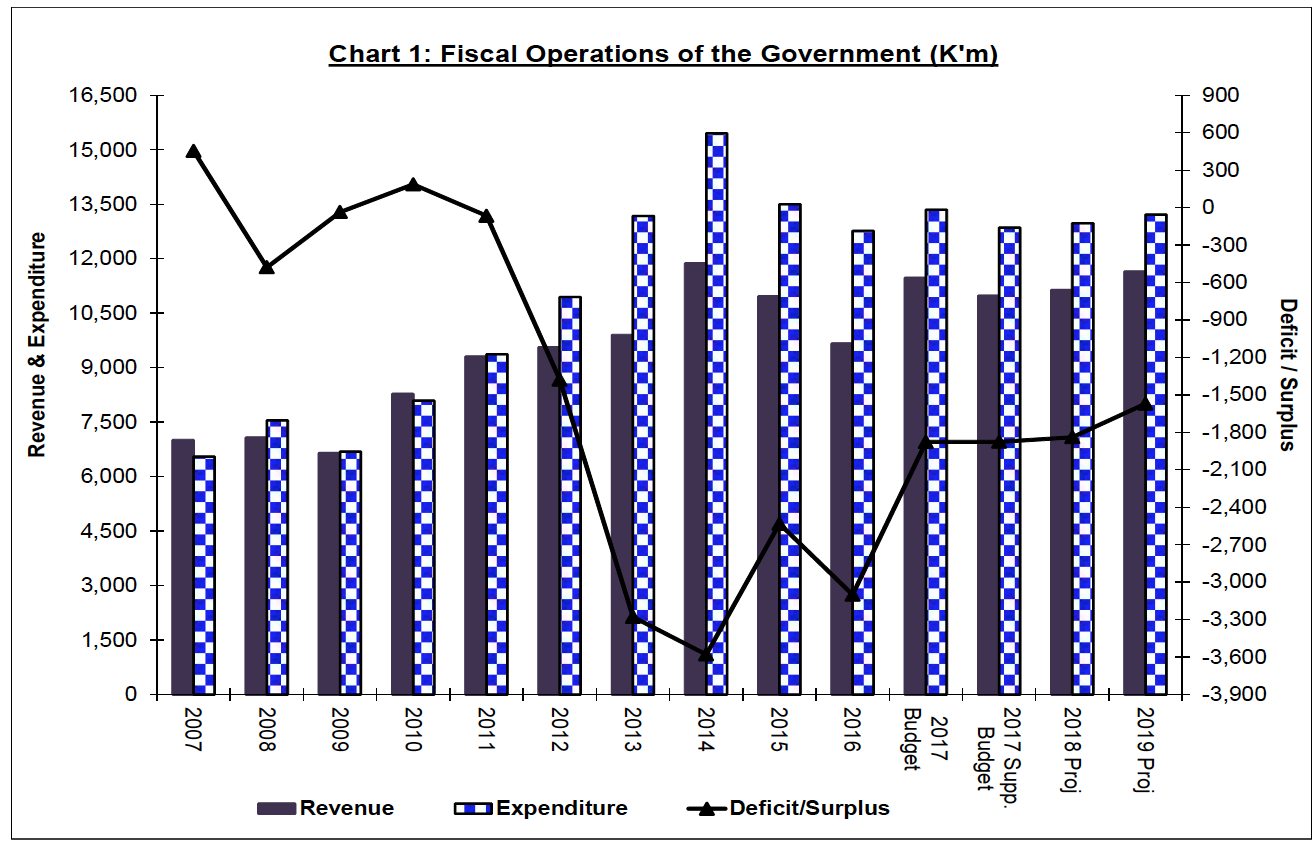

PNG government’s fiscal operations. Source: BAPNG

According to Moody’s, over ‘the next few years’ the PNG government’s gross borrowing requirements will ‘remain large’ at about 16-17 per cent of GDP.

‘The confluence of rising government debt, albeit from low levels, a large share of shorter-dated and high interest rate domestic maturities, and increasing reliance on external commercial debt will continue to weaken debt affordability and weigh on overall fiscal strength,’ the report says.

‘Until recently, PNG’s large superannuation funds and banks contributed to a reliable source of financing.’

‘In turn, persistent liquidity constraints raise refinancing risks.’

Domestic financing sources

The Moody’s report observes that, until recently, PNG’s large superannuation funds and banks contributed to a reliable source of financing.

The government’s ‘sizeable fiscal deficits’ since 2013, however, have strained the domestic financial system’s ability to absorb government borrowing.

‘Prospects for further domestic financing are constrained as some banks are reaching internal limits for holding government securities.

‘The tightening conditions are making it harder for Moody’s to raise long-term debt.’

‘Deteriorating government liquidity is manifesting in higher local interest rates, which feeds into weaker debt affordability.’

The report predicts that interest payments will absorb 15.1 per cent of government revenues in 2018. ‘[This is] higher than many similarly-rated sovereigns, and up sharply from recent years.’

The tightening conditions are making it harder for the government to raise long-term debt, according to Moody’s.

‘To the extent that domestic investors are still willing and able to purchase government securities, demand is shifting to shorter maturities, which raises refinancing risks.

‘Treasury bills with maturities of less than one year account for around 39 per cent of all government debt in 2017, up from 32.4 per cent in 2012 and 15.6 per cent in 2007.

‘The Bank of Papua New Guinea is absorbing a greater share of government bonds to help offset weakening domestic investor appetite.’

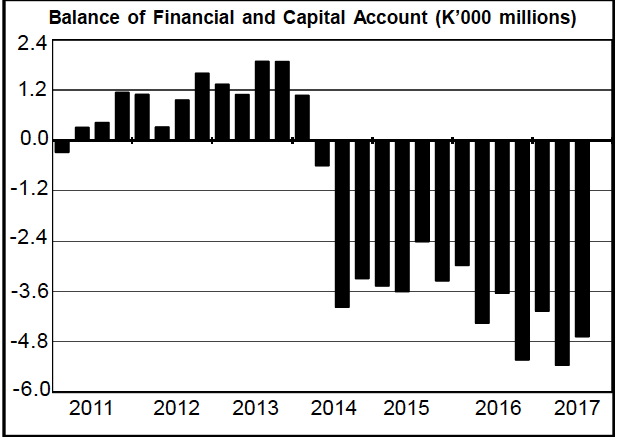

PNG’s financial and capital account. Source: BAPNG

Constraints

The Moody’s report predicts that the government will respond to the greater financing constraints by relying more on external market debt. But it says that this strategy carries risks if the kina depreciates.

‘Rising external debt will leave the debt burden and debt servicing costs more vulnerable to a potential local currency depreciation and higher interest rates.

‘External debt repayments will rise from 2020.’

‘Moreover, external commercial loans typically face higher interest rates than concessional loans, which will further contribute to rising debt servicing costs.

‘Pressure on external debt servicing costs in the next couple of years is partly offset by the still sizeable proportion of the government’s debt stock that is based on concessional terms.

‘But external debt repayments will rise from 2020 as repayments on commercial external loans come due.’

Expenditure

Cutting expenditure has in the past been the way the government has dealt with financing difficulties, the report notes.

But it argues there is only limited scope to reduce expenditure further, from the 2017 level of 18 per cent of GDP.

‘In the near term, liquidity pressure may lead to a further build-up of arrears.’

Longer term, fiscal reforms and technical support from international financial institutions will enhance the conduct of fiscal policy.

The Moody’s report does make some hopeful observations. It points to the development of the 2018-2022 Medium-Term Revenue and Fiscal Strategy, as a positive move.

‘[The Strategy] provides new fiscal anchors that, if successfully adhered to, could allow the government to rebuild fiscal buffers that can help mitigate the impact of potential future negative shocks.

Moody’s predicts government debt will rise to around 34 per cent of GDP by 2019, up from about 32 per cent in 2017.

This will leave the government with limited fiscal flexibility ‘in the event of a significant negative economic shock’.