What Papua New Guinea’s central bank is saying about the economy

Ahead of this week’s expected Supplementary Budget, the Bank of Papua New Guinea’s September Monetary Policy Statement points to continued financial pressures, despite a strong trade performance. David James considers what it means for foreign exchange and domestic demand.

Bank of Papua New Guinea building in Port Moresby. Credit: BAI

The divergence between Papua New Guinea’s trade, which is strong, and the financial sector, which is under stress, continues.

The Bank of PNG statement says the country’s export performance was robust. There was a surplus in the current account because of ‘higher production and favourable international prices for most of the major export commodities.’

But that strong trade performance was offset by continued financial outflows due to ‘higher external debt service payments by the mineral companies and the government’ and investments abroad by mineral companies.

Budget deficit

The government’s accounts are also under pressure. The document says the national government in the first half of 2019 recorded a budget deficit of K1.67 billion, more than four times the deficit in the same period of 2018 of K324.9 million. The deficit for 2019 is projected to widen by K506.4 million to K2.37 billion.

‘The high deficit is a concern as the Government is facing challenges in raising sufficient revenue and other sources of financing to fund the high expenditure level. A prudent fiscal strategy implemented through a supplementary budget would be necessary to align expenditure to revenue.’

‘If the high debt and expenditure do not translate to high economic growth, this will raise serious concerns about the sustainability of debt.’

It is anticipated that the Supplementary Budget, due to be delivered tomorrow, will incorporate some funding from external sources, with the PNG Government having held talks with some foreign governments and international finance institutions in recent months.

According to the statement, growth in government tax revenue has been ‘stagnant’ in the post-LNG period (2014 to 2018) despite strong growth in GDP. The Bank points to persistent problems in collecting sufficient tax.

The low tax revenues have in large part been due to tax credit schemes and other concessions given to companies, says the report. Meanwhile, government expenditure ‘continues to remain in excess of revenue’, adding that slippages in expenditure have become frequent, ‘partly reflecting front loading of expenditure through borrowing in anticipation of future LNG revenues.’

It says that funding has been diverted from ‘productive areas to consumption’ and that this has restricted investment in economic infrastructure. The resultant large Budget deficits has forced the government to resort to continuous borrowing, increasing the overall debt level.

‘If the high debt and expenditure do not translate to high economic growth, this will raise serious concerns about the sustainability of debt.’

Total Government debt has increased from K25.6 billion in December 2018 to K27.4 billion by June 2019.

Foreign exchange

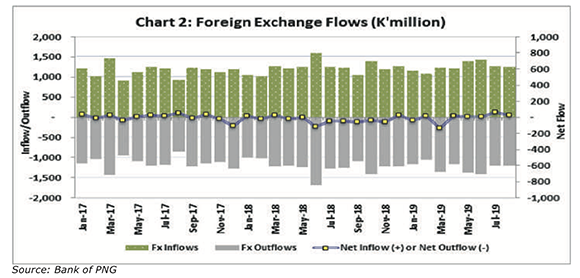

The statement suggests that the foreign exchange shortages have improved, partly because the government sought financing internationally (the sovereign bond). Inflows from mining companies also increased and the backlog of orders was further reduced because of Bank of PNG’s interventions.

‘The average time taken for orders worth K3 million and above to be cleared has reduced from six months in 2018, to less than three months in 2019. These are positive developments in terms of meeting the foreign exchange requirements of the private sector and PNG’s development needs.

Foreign exchange flows in kina from 2017 to July 2019. Credit Bank of PNG

‘Most of the foreign exchange inflows have been served to the retail, manufacturing and finance and business sectors. The level of gross foreign exchange reserves was US$2.04 billion (K7.07 billion) as at 30th June 2019, compared with US$2.3 billion (K7.45 billion) at the end of December 2018. This level is sufficient for 5.3 months of total, and 11.3 months of non-mineral, import covers.’

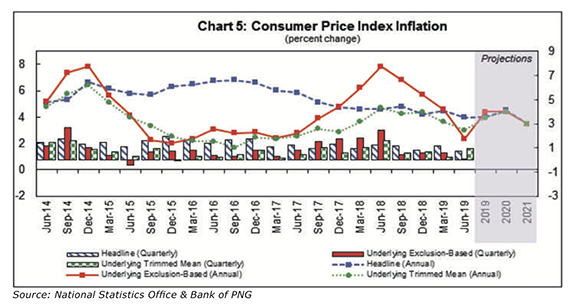

The Bank projects annual headline inflation to be about 4.5 per cent in 2020 and 3.5 per cent in 2021. It says it will maintain an ‘easing stance’ of policy in the next six months.

The bank projects GDP growth for 2019 (after inflation) to be 4.4 per cent – driven by continued strong exports.

‘The primary driver of this growth continues to be the rebound and full year production and export of LNG, crude oil, condensate and gold, which were severely affected by the earthquake in February 2018.’

Broad money supply contracted by four per cent in 2018 and by 3.5 per cent in the first half of this year (the bank’s forecast was for positive 3.5 per cent for this year). This suggests that spending demand is under pressure, pointing to a weak domestic economy.

What this may mean for business

-

Financial stresses will remain, despite strong trade statistics. Without an influx of new foreign capital the economy will continue to be under pressure.

-

Monetary policy is being eased and inflation pressures seem to be under control.

-

The weakness in money supply suggests demand in the domestic economy may be weak.