Papua New Guinea experiencing temporary loss of momentum, say reports

With experts forecasting slow economic growth in 2020, Papua New Guinea’s economy may be facing a temporary loss of momentum. David James examines two new economic reports and what they may mean for business.

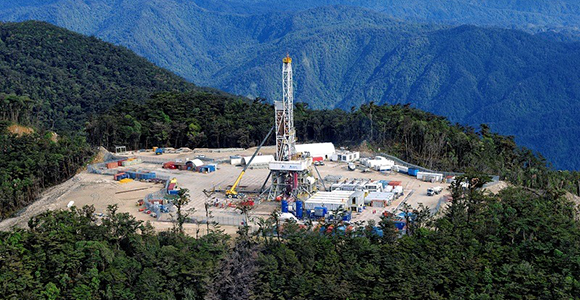

Hides well pad, part of the PNG LNG Project. Credit: Santos

Economists’ forecasts for PNG’s growth are being lowered, indicating growing pessimism about the year ahead.

The latest outlook for PNG produced this month by rating agency Fitch Solutions forecasts a growth of 3.3 per cent in 2020, down from an estimated 4.5 per cent in 2019 ‘as recent base effects fade and uncertainty remains over the development of major LNG and mining projects.’

This compares with the two percent GDP growth for 2020 presented in PNG’s National Budget.

The Fitch report claims this will be a ‘temporary loss of momentum’. When and if resource deals such as Papua LNG, P’nyang and Wafi-Golpu are finalised, growth is expected to accelerate from 2021, leading to a surge in investment and exports.

For 2020, however, economic weakening is expected, with ‘sluggish growth in fiscal revenues and a softer expansion in private credit’. These are trends Fitch expects to remain in place over the coming quarters.

Business confidence

The report also notes that there has been a slowing of the increase in commercial banks’ outstanding loans. This, it says, is ‘a symptom of lower business confidence amid political instability [due to] a change of government in May [2019], the subsequent uncertainty over the future of key resource projects, and ongoing shortages of foreign currency.’

The Fitch report claims, however, that if the major resource projects get the go-ahead the economic growth prospects for PNG could be strong.

‘Low confidence – due to delays in accessing foreign currency and uncertainty surrounding the next round of mega-resource projects – is not encouraging firms to invest.’

‘We expect GDP growth to accelerate to 4.2 per cent in 2021 and 4.6 per cent in 2022, before rising further to average above 6 per cent a year once major resource developments come online.

‘However, we note some downside risks from political uncertainty, particularly surrounding the future of the Bougainville region following its recent vote in favour of independence, as well the potential for unexpected government policy changes related to resource extraction in the country.’

Bearish

A more bearish assessment comes from the ANZ, in its economic outlook for Papua New Guinea, released last month. The bank is forecasting GDP growth of only 1.9 per cent in 2020, down from an estimated 3.6 per cent in 2019. Inflation (the Consumer Price Index) is predicted to increase by 4.5 per cent, meaning that real economic growth is expected to be negative.

‘We anticipate the economy will remain soft in 2020, largely due to ongoing weakness in construction, in particular mining investment,’ the report says.

‘Non-mining business investment remains subdued. With weak demand and weak profits, it doesn’t make sense for businesses to invest, especially when many still have excess capacity.

‘Low confidence – due to delays in accessing foreign currency and uncertainty surrounding the next round of mega-resource projects – is not encouraging firms to invest.’

[infogram id=”anz-report-1h8n6m1yy7zg6xo” prefix=”i68″]

Sectors

The ANZ report points out that many of the economic levers available to government and the central bank have only a limited effect.

Monetary policy (the easing of interest rates) is not ‘stimulating demand’, fiscal policy options (government spending) are limited because the government is ‘up against its debt limit’ and, with the delay in the negotiations over P’nyang, no increase in foreign direct investment is anticipated.

‘If the (P’nyang) negotiations can be completed within agreed deadlines, we believe a recovery will come in the second half of 2021 – a year later than anticipated.

‘Obviously, a longer project dialogue will push the recovery out further, with a risk that extended negotiations could derail the economic upturn.’

The bank maintains its view that the next round of investment in extractive industries (Papua LNG, PNG LNG expansion, Wafi-Golpu and the Sepik Development Project) will trigger a ‘super cycle’ of investment and an economic boom in PNG. If they go ahead.

What this may mean for business

- Short-term strategies should focus on controlling costs given the likelihood of weak demand and slow overall growth.

- Confidence is likely to remain weak until well into 2021, which implies that profit margins will be tight and gains are more likely come from increasing market share.

- The medium term prospects for the PNG economy are positive if resources projects go ahead. However, these will require a rethink of business strategies.