Ratings agency reveals how Papua New Guinea will manage its debt

Papua New Guinea’s Government is set to rely heavily on concessional finance from multilateral institutions, according to ratings agency Moody’s. The agency is maintaining a B2 rating for PNG debt but has some surprising revelations about the country’s finances.

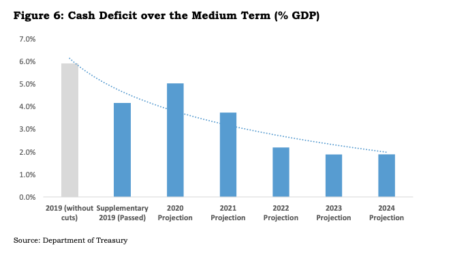

PNG’s projected cash deficit. Credit: Department of Treasury

Moody’s latest credit opinion, released earlier this month, says the B2 rating affirmation depends on the expectation that there will be a ‘mobilization of external financing resources’, which will ‘mitigate’ financial challenges being faced by the government.

It describes the anticipated financial position of the government (fiscal trajectory) as weaker than previously expected, pointing to a probable lack of cash to meet obligations (liquidity shortages).

The Moody’s report notes that efforts by the Marape government to improve the transparency and accountability of PNG government finances – last year’s ‘review of PNG’s fiscal landscape’– will help improve the country’s international standing.

That initiative, it says, has ‘established a comprehensive economic and fiscal reform program’ that is expected to foster ‘greater adherence to fiscal rules, increased fiscal transparency, and stronger commitment towards maintaining macro-fiscal stability, while taking into account the likely implementation challenges.’

The report also points to the International Monetary Fund’s staff-monitored program for PNG, announced last month, which it describes as a ‘policy anchor’ that will help the government mobilise ‘greater amounts of external, concessional [low interest] financing,’ and help the PNG government contain ‘liquidity risks’.

Concessional financing

PNG’s Treasurer Ian Ling- Stuckey [left] and ADB President Nakao. Credit: ADB

Such financing, the report says, will ‘help enact reforms in areas of public financial management, state-owned enterprise governance, and monetary and exchange rate reforms and raise PNG’s external financing over 2020-21.’

‘PNG’s debt burden is expected to increase to about 45 per cent of GDP in 2020-21, up from an estimated 40 per cent of GDP at the end 2019.’

With words that will buoy businesses currently waiting up to eight weeks for foreign exchange, Moody’s suggests such financing will also support ‘greater economy-wide foreign exchange availability.’

Borrowing

The Moody’s report indicates that the short term stresses on the National Budget are severe. It predicts that the government’s annual gross borrowing requirements will peak at approximately 20 per cent of GDP in 2020, before gradually declining to around 15 per cent of GDP by 2022-23.

PNG’s debt burden is expected to increase to about 45 per cent of GDP in 2020-21, up from an estimated 40 per cent of GDP at the end 2019.

Debt affordability, as measured by interest payments as a share of revenue, is expected to weaken over the same period. ‘PNG’s fiscal position will remain broadly in line with similarly-rated sovereigns.’

Forecasts

The report provides several forecasts for the PNG economy:

- Real GDP growth of ‘just 1.1 per cent’ in 2020 and 2.3 per cent in 2021, reflecting ‘renewed delays in construction and foreign direct investment flows from large resource projects entering final investment decision (FID)’.

- Inconclusive negotiations for development of the P’nyang gas field that will result in delays of the development of the Papua LNG and the PNG LNG extension projects, ‘given synergies across the projects’.

- Greater exchange rate flexibility that will result in downward pressure on the kina, which should be ‘contained’ and is ‘unlikely to result in a large increase in the debt burden’.

- Greater fiscal discipline and gradually reoriented expenditure towards facilitating growth in the non-resource economy.

- A commitment by the government to limit the growth in public sector emoluments, preventing any ‘further build-up in domestic payment arrears.’

The report says the local currency bond and deposit ceilings will remain unchanged at Ba2. ‘The foreign-currency bond ceiling is unchanged at B1 and the foreign-currency deposit ceiling is unchanged at B3.’